December 12, 2024

Hello there,

Welcome again to any newcomers!

This is our biweekly newsletter where we talk venture capital, Connetic, data, and sometimes funny stuff. Hope you enjoy and read to the end!

It’s basketball season and with the Bengals struggles it couldn’t come soon enough! We root for 3 teams in my house, with our kids currently attending UK, NKU and UC. I love them all but one is a little more near and dear to my heart. As a graduate from UK I just can’t help it. Here’s what’s funny though, I have been taking my middle daughter Andie to the opening UK game since she was 4 years old, and turns out, she’s the one that went to UC! That’s ok because she still attends the UK games with me. One day a year on parents weekend, I can stomach putting on my UC gear and enjoy the festivities there too.

Today’s article is a good one! I have an interesting content piece on liquidity, a new monthly fact card, and, if you read to the end, you can see Mark Pope calling the ending play against Duke, so amazing!

Keep reading to get all the updates and more below!

In today’s update:

- Why are we so obsessed with liquidity?

- Data: What’s up with car loan delinquencies?

- Venture News

- Connetic Corner: JD is moving to KY and Platform News

- Super Interesting Reads:

- A.I. Jesus

- Pentagon fails audit, again.

- Small wins by Roger Federer

- Stuff That’s Cool AF: Coach Pope v. Duke

- Fact Card: November 30

By: Brad Zapp, CFP®,

Portfolio Manager, SVP

Why are we so obsessed with liquidity?

In the U.S., liquidity isn’t just about having cash; it’s a badge of financial security, a sort of “I’m ready for anything” superhero cape. You might say it’s the financial equivalent of carrying around 14 varieties of Band-Aids in your purse—sure, you’re ready for every kind of paper cut or blister, but are you really going to need all that? Americans have a long-standing tradition of needing control over their cash, stemming from cultural norms that value independence, fast action, and self-sufficiency. This mentality, reinforced by advisors and financial talk shows, puts liquid assets on a pedestal like they’re a universal solution to every life event, from medical emergencies to “great opportunities” in late-night infomercials.

The American penchant for liquidity has also been driven by turbulent events like the 2008 financial crisis and the COVID-19 pandemic. In times of economic uncertainty, cash is king, and so Americans have been taught to stash it away as if the next disaster is lurking right around the corner. But while having quick cash can indeed help in a crisis, obsessing over liquidity may lead people to undervalue assets that could bring greater returns over the long haul.

Economic Factors Driving Liquidity Preference

Aside from cultural influences, American liquidity fixation is also tied to economic factors. The U.S. has a consumer-driven economy that, like a goldfish, will grow to fit the size of the bowl it’s given—and Americans do their best to make that bowl huge.

With a national love of quick purchases and convenience, Americans often prioritize liquid assets simply because they feed into the next exciting purchase. Liquidity, to many Americans, means being able to respond to a flash sale at the mall or to take advantage of “limited time only” offers that seem, oddly enough, to never truly end.

The Downsides of Overemphasizing Liquidity

- Missed Opportunities for Long-Term Growth

Constantly worrying about liquidity is a bit like keeping all your money in quarters in a piggy bank “just in case.” Sure, you’ll always have change for the parking meter, but meanwhile, your friends who invested in a property five years ago are now paying their mortgages with the rent checks they receive. When investors fixate on liquid assets, they often miss out on higher-growth, illiquid investments like real estate, venture capital or private equity, which we believe have the potential to offer better returns. In the pursuit of instant access, Americans may sacrifice financial growth, not unlike how someone who only eats instant noodles misses out on the joys of a home-cooked lasagna. - Inflation Erosion of Cash Reserves

Keeping large cash reserves to protect against uncertain times has an unexpected downside: inflation. It’s a little like storing up Halloween candy and realizing in March that half of it has turned stale and unappealing. With inflation chipping away at the purchasing power of cash, those large reserves lose value over time. Americans, who prioritize liquidity to be “safe,” might not realize they’re just letting their money sit in a slow cooker of depreciation. When inflation rates outpace the interest in savings accounts, it’s like watching your cash evaporate, one penny at a time, into the foggy ether of economic caution. Consider this, a $100,000 investment in cash or cash alternatives in 2019, after accounting for a 20% tax on interest and 20% cumulative inflation from 2019 to 2023, the account would have an after-tax value adjusting for inflation, the purchasing power would be approximately $90,272, roughly a 10% LOSS.*

Neglect of Productive Illiquid Investments

When investors focus solely on liquidity, they often avoid potentially advantageous illiquid assets like venture capital, private equity, real estate, or even art—asset classes more appreciated abroad. Picture an Italian investor admiring their family’s vineyard, or a Japanese businessperson holding shares in a family-owned company that’s been passed down for generations. Meanwhile, in America, a focus on liquidity means many investors are more likely to own shares in a public company they don’t understand than to build long-term value in a more tangible asset. By prioritizing liquidity, Americans may miss out on potentially rewarding investments that require patience, such as buying a property and watching it appreciate or investing in a private company that one day goes public.

Why Americans Might Reconsider Their Liquidity Focus

While liquidity undoubtedly has its place (it’s hard to pay for emergency car repairs with a priceless Renaissance painting), a more balanced approach could provide greater financial stability. Alongside holding assets in accessible cash or liquid stocks, Americans might explore investments that require a longer commitment and offer the potential for enhanced returns. Imagine turning off your phone, so to speak, to let your investments simmer undisturbed in a slow cooker instead of microwaving them every few minutes to “check on them.” Long-term wealth-building doesn’t require constant oversight but rather a calm, disciplined approach that may be hindered by the temptation of liquid assets.

A shift in mindset could also lead to a more measured approach to spending. When every dollar is liquid, it’s easy to justify using it on “fun” purchases or impulsive investments. By investing in illiquid assets, individuals might be more inclined to think strategically about their finances, understanding that certain funds are meant to grow quietly in the background rather than to be accessed for an impulsive shopping spree.

*For illustrative purposes only. It does not represent actual an actual investment, and is not investment advice, nor a forecast or guarantee of future results. Illustrations of hypothetical principles have inherent limitations and cannot account for future economic conditions. Results may vary.

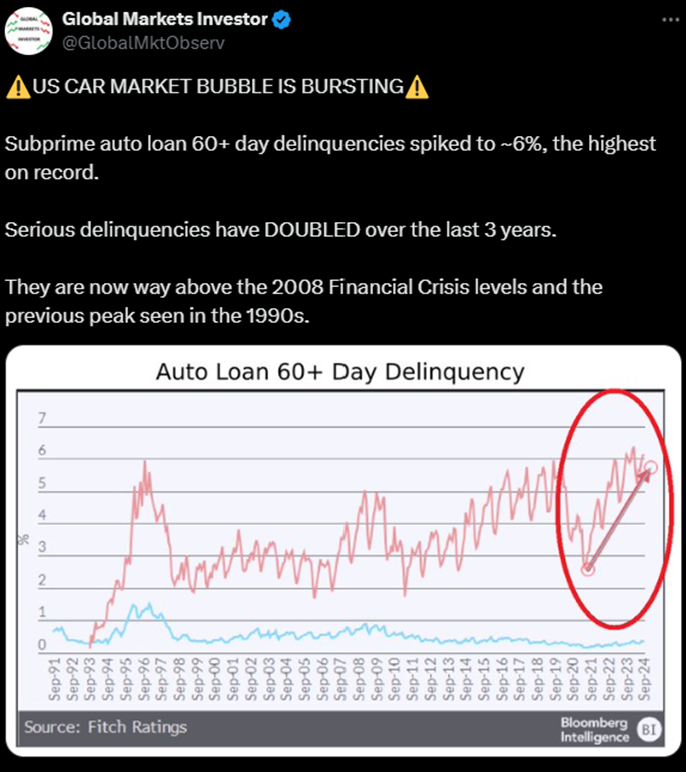

Data – What’s up with car loan delinquencies?

Source: original data Fitch/ post on X by @globalmktobserv

This looks bad. Should we worry?

Data – AUM & Portfolio Count (as of December 11, 2024)

Venture News

Fund Activity

- New Investments:

We are pleased to announce the first two new investments under the fund:

This brings our total number of positions in the fund to 141. We are well diversified and this has been a point of emphasis and differentiation as we’ve conducted investor meetings over the last month.

- Follow-On Investments:

In addition to the new investments, we have completed follow-on investments into three of our existing portfolio companies to further support their growth and scalability.- Base Social an in real life social company

- Cloud Range Cyber Series A Cyber Security

- Narratize an A.I. Seed Round

- Deal Sourcing

Since effectiveness, we have seen a large uptick in deal flow, 40% MoM growth, and have a healthy pipeline of companies in diligence.

Our diligence pipeline has over 20 opportunities at this time.

For more details, please visit our Fund’s website at www.conneticventures.com/vcafx. On the website, you’ll find updated SEC filings and the most recent fact card.

Fund Accessibility and Distribution Updates

- Public Accessibility:

Our ticker is now live and can be accessed on traditional finance websites like Morningstar.com*. We are currently working with our administrator to pull updated data on core strategy and investments into Morningstar for broader visibility. - Advisor Platforms:

We are now available for electronic trading through advisors who custody their assets on Axos. (If you are an advisor and looking to add a custodian, let me know).

- We are also available through Broadridge Matrix who powers the Inspira/Millennium Trust platform for electronic trading.

- We are also working through a selling agreement with SEI Trust that powers trust accounts for financial advisors.

- We are working on others, I call this process, getting the plumbing in place. If you have a financial advisor ask them to meet with us, or ask them to get your holdings on your platform. It takes a village, and I will tell you, this is an asset class that is a point of emphasis at many brokerage firms and custody platforms.

* Past performance does not guarantee future results. Short-term performance is not a good indication of the Fund’s future performance and an investment should not be made based solely on returns. Performance shown is net of fees.

JD is here, Christmas is coming, our holiday party is behind us, so what’s happening…. a lot actually! We will not be idle and mindlessly walk to the new year, we have to get ready for our auditors. Their work will begin January 2nd in order to best meet the SEC timeline which is now shortened from 90 days to 60 days for audited financials post fiscal year end. That is no small task, but we are all up for the challenge. We also are working to get some more deposits before year end. This is our first quarter, we have an obtainable goal of $1M of in flows and we are almost there. If you can help us achieve that, please do so. These signals are important. The coolest thing that happened recently was we had our first portfolio company Founder/CEO turn around and invest in our fund. Mike Preuss, of Visible. Think about that for a minute. He was amazed at the simplicity and convenience, loved that there was no future capital calls, and that he could invest with an amount he could currently afford. He had never had the opportunity to invest cash indirectly back into his own company and the other startup opportunities until now. I love that, and I hope more follow his lead. I’ve said it the last couple newsletters, but we need your help. To make that easier, we are ready to roll out your online portal! You will be getting an email next week for you to setup your account. I know there is about 10% of you, that still think the internet is a fad, but I’m sorry, its here to stay and you will love seeing your accounts move everyday. Don’t forget to hit that ‘invest more’ button 😉

If you need anything else, email or text me. Also, we will be skipping 1 newsletter cycle and will return again Thursday, January 9th. The goal between now and than is to get your online accounts setup.

Big days ahead!

Super Interesting Reads

Holy Tech! AI Jesus

Pentagon Fails Audit, Again. Pentagon Audit Failure

Morningstar.com, small wins can add up. By Roger Federer for the win

Cool AF of The Week

I know it was like a month ago, but if you haven’t seen Coach Pope predict the end, this is freaking awesome!

|

Thanks for reading!

Please get to know a few firms we simply LOVE working with.

See attached Fact Sheet for additional important information, including the Fund’s top 10 holdings.

Share using the buttons below

Follow Us

Note: This newsletter is for information purposes only, and does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service referenced herein.

Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectus contains this and other information about the Fund and can be obtained by calling 1-800-711-9164 or by visiting the Fund’s website at https://www.conneticventures.com/vcafx. Please read the prospectus carefully before investing. All investments involve risks, and past performance is no guarantee of future results.

The content herein is for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation in respect to any products or services for any persons who are prohibited from receiving such information under the laws applicable to their place of citizenship, domicile, or residence.

Some statements herein may express future expectations and forward-looking views based on Connetic’s current assumptions. Statements about companies, securities, or other financial information represent personal beliefs and viewpoints of Connetic or the respective third party. These statements may involve known and unknown risks and uncertainties, potentially leading to different results than those implied or expressed. All content is subject to change without notice.

The Connetic Venture Capital Access Fund (the “Fund”) was organized as a Delaware statutory trust on September 11, 2023, under a Certificate of Trust governed by the laws of the State of Delaware. The Fund acquired all of the assets and liabilities of 908 Investments LLC (the “Predecessor Fund”), a private fund that merged into the Fund, in a tax-free reorganization on October 2, 2024 (the “Reorganization”). In connection with the Reorganization, interests in the Predecessor Fund were exchanged for Class I Shares of the Fund. The Predecessor Fund had an investment objective and strategies that were, in all material respects, similar to those of the Fund and are managed in a manner that, in all material respects, complies with the investment guidelines and restrictions of the Fund. Connetic RIA LLC (the “Adviser” or “Connetic”) managed the Predecessor Fund.

The Fund is a diversified, continuously offered, closed-end management investment company designed for long-term investors. The Fund is neither a liquid investment nor a trading vehicle.

- Shares are not listed for trading on any securities exchange, and you should not expect to be able to sell Shares in a secondary market transaction. You should consider Shares of the Fund to be an illiquid investment.

- Shares are not redeemable at the shareholder’s option. The Fund does not intend to offer to repurchase Shares until January 2025. At that time, the Fund will offer to redeem no less than 5% of its outstanding Shares four times each year.

- The Fund has no intention to repurchase Shares outside of these quarterly repurchase offers that will begin in January 2025, and these repurchase offers may be oversubscribed.

- If you tender your Shares for repurchase as part of a repurchase offer that is oversubscribed (i.e., because more than 5% of the Fund’s outstanding Shares are tendered for repurchase), the Fund will redeem only a portion of your Shares.

- Because Shares are not listed on a securities exchange, and the Fund will only offer to redeem no less than 5% of its outstanding Shares four times a year starting in January 2025, you should not expect to be able to sell your Shares when and/or in the amount desired, regardless of how the Fund performs. As a result, you may be unable to reduce your exposure to the Fund during any market downturn.

- The Fund is designed for long-term investors. An investment in the Fund may not be suitable for you if you need the money you invest within a specified period.

- The amount of distributions the Fund may pay, if any, is uncertain. There is no assurance that the Fund will be able to maintain a certain level of distributions to shareholders. A portion or all of Fund distributions may consist of a return of capital. Any capital returned to shareholders through a distribution will be distributed after payment of fees and expenses. A return of capital distribution will not be taxable but will reduce the shareholder’s cost basis and result in a higher capital gain or lower capital loss when those shares on which the distribution was received are sold. Once a shareholder’s cost basis is reduced to zero, further distributions will be treated as capital gain if the shareholder holds shares of the Fund as capital assets.

- The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as from offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors.

- The Fund’s investments may require several years to appreciate in value, and there is no assurance that such appreciation will occur.

- Investing in the Shares may be speculative and involve a high degree of risk, including the risks associated with venture capital investing and the potential loss of your entire investment. See “Risks” in this prospectus.

The Fund is distributed by Foreside Financial Services, LLC.

Connetic RIA, LLC, 910 Madison Ave, Covington, KY 41011