February 26, 2025

Hello there,

Welcome again to any newcomers.

This is our biweekly newsletter where we talk venture capital (“VC”), Connetic, data, and sometimes funny stuff. Hope you enjoy and read to the end!

I just returned from my first (as a VC) financial advisor conferences, and forgot how much I missed them. I was invited to speak at the United Advisor Group 2nd annual conference in Tempe, AZ. First, I have never been to Tempe for a stay. It was cool. College campuses are always lively. Speaking of lively, Scottsdale was a short Waymo ride away, hosting the Waste Management Open, which yes, I went to. First back to Tempe, it has great beauty. It has these “mountains”, but I think they are more like giant hills, either way, they are cool. I took Friday afternoon to summit the peak of the Great A Mountain with my buddy, Brad Willits (iCapital). Then I stepped into my first driverless car, it’s a service called Waymo. Look, my first ride was a bit shocking to my system with the no driver thing and all, but I quickly realized how amazing it was compared to Uber. You control EVERYTHING, you can do ANYTHING, and no pressure to talk or listen to the driver’s music selection. You can take a call in private, and the cars are all very nice. It’s like the ‘spa’ experience of taxis. I told my wife the day Waymo comes to Cincy I’m selling my truck and taking Waymo everywhere! Last thing I’ll say about my trip, back to the financial advisors, it was awesome to be a small part of their annual meeting and listening to them and the other vendors. It reminded me what vital service these men and women play in our financial lives. I got to know a few of them pretty well over the few days I was there and I even talked one, Brian Yeakley and his wife Marissa, into joining me in a suite on the 16th tee (hard sell I know – great thanks to my friend Jim Barresi at Squire Patton Boggs for the seats). Lots to chat this week.

- In today’s update:

- Investing is Not Monopoly & the Low Correlation Superhero

- Data: Mortgage Rate Prison?

- VCAFX and Portfolio News

- Connetic Corner: Tax Season

- Interesting Reads:

- Stay Ahead of Your Wealth

- Why Investors Fail

- Cool AF: Mark Pope “Godfidence”

- Fact Card

By: Brad Zapp, CFP®

Portfolio Manager

Investing is Not Monopoly & the Low Correlation Superhero

Investing is like dieting: you don’t gain weight just by looking at pizza, and you don’t lose it by dreaming about kale. Yet, when it comes to investments, clients often behave as if a single dip or rise in the market is a life-altering event. “I lost money this month!” they exclaim, or, “I made money this month!” Reality check: stock prices are not Monopoly money you cash in every time the dice rolls in your favor.

Here’s the truth: market prices aren’t realized gains or losses. They’re appraisals—fancy market guesses about what your assets are worth if you sold them today. So, let’s break down why I believe these mental accounting gymnastics are not only wrong but could also be the reason your financial life feels like an endless loop of “Go Directly to Jail” cards.

Stock Prices: Zillow for Your Investments

Think of stock prices like Zillow’s estimates for your house. They’re an appraisal, not a finalized check in your mailbox. You wouldn’t say, “I lost $100K today because the neighbor sold their house for less.” You’d roll your eyes at the market and move on. Similarly, just because your portfolio dropped 5% doesn’t mean your future yacht is now a dinghy. You haven’t lost money until you sell.

Why does this distinction matter? Because obsessing over every tick of the market turns your long-term financial strategy into a melodrama that even soap operas would envy.

Why Do We Fall for This Trap?

It’s called loss aversion, or as I like to call it, “financial hypochondria.” People feel the pain of a 10% loss way more than the joy of a 10% gain. For example:

- If your portfolio loses $50,000, you’re in a fighting mood, you know you have typed that email to your advisor ten times already.

- If it gains $50,000, you shrug, maybe buy a fancier latte, and move on, totally ignoring it.

The human brain is wired to overreact to perceived losses, and when you pair that with a constant stream of market updates, it’s no wonder people feel like they’re on an emotional rollercoaster. Recently, I heard some sage wisdom from a financial advisor, Tony Fiorillo, Managing Partner of Asset Mgmt. Strategies Inc., “Brad do you fear your scissors and knives in your drawer?

Me: “No I don’t…”

Tony: “Why not, don’t you know they are sharp?”

Me: “Yes, but I don’t touch, use or even look at them everyday.”

Tony: “Good way to treat stock market news.”

I thought that is brilliant, you know who said something VERY similar? Warrant Buffet, he said “…ignore the stock market, it does not even exist.”

Low Correlation to the Rescue: The Superhero of Risk Management

Want to sleep better at night while ignoring those dramatic market swings? Enter low-correlation assets—investments that don’t all move in the same direction at the same time. Think of them as the peanut butter to your portfolio’s jelly.

When stocks zig, the old adage was bonds often zag, (maybe not anymore see article: Bonds don’t belong) creating balance and reducing your portfolio’s volatility. It’s like hiring a team of superheroes instead of relying on 1 caped crusader—because let’s face it, Batman can’t fix everything.

By combining assets that don’t move in lockstep, fiduciaries (your financial advisors) can create a portfolio that helps to weather market conditions, reducing overall risk while preserving growth potential.

Here’s why ignoring correlation is a catastrophic mistake:

- Failure to Protect Against Systemic Risk:

During a market crash, many asset classes with low volatility (like certain bonds) may still move in the same direction as equities. Without uncorrelated assets, such as commodities or alternative investments, the entire portfolio can sink together. Fiduciaries who fail to consider correlation risk leaving clients unprepared for systemic events. - Missed Opportunities for Growth and Resilience:

Low-correlation portfolios thrive on diversification. For example, pairing equities with assets like real estate, international stocks, or inflation-protected securities have the potential to reduce volatility without capping gains. This approach help to ensure that no single market event derails the client’s financial plan. - Behavioral Challenges Amplified:

When fiduciaries ignore correlation and overweight low-volatility or buffered products, they unintentionally reinforce clients’ short-term thinking. Clients may feel safe but become disillusioned when they realize their portfolios are underperforming their peers. This increases the risk of panic-driven decisions, like abandoning the advisor altogether.

Financial Advisors Wake UP!

The Hidden Danger of Ignoring Correlation: Why Overweighting Low-Volatility or Buffered Products Is a Fiduciary Risk

Imagine building a fortress for your client’s financial future and forgetting to include doors. I believe that’s what happens when fiduciaries prioritize low-volatility or buffered products at the expense of low-correlation investments. These products may seem like the “safe” choice, but focusing too heavily on them has the potential to leave portfolios vulnerable to the very risks fiduciaries are sworn to mitigate. In this essay, let’s expose the dangers of this misguided behavior and scare some sense into advisors who undervalue the power of correlation.

- Your Reputation on the Line: Clients start comparing their underperforming portfolios to their neighbors’ diversified investments. Trust erodes, and your practice suffers irreversible damage.

Now imagine the alternative: you prioritize low-correlation investments. During downturns, your clients see the benefits of diversification as one asset class cushions the blow from another. Their portfolios grow steadily, and they trust you more for helping them stay on track.

Conclusion: The Fiduciary Imperative

Fiduciaries have a duty to act in their clients’ best interest—not their emotions. Overweighting low-volatility or buffered products is a short-term bandage that risks long-term harm. Instead, embrace the power of low correlation. Diversify thoughtfully, reduce systemic risk, and help to ensure clients’ portfolios can weather any storm while still reaching their financial goals.

Focusing on correlation isn’t just good advice in my opinion—it’s your professional responsibility. Clients: Don’t be with an advisor who drives the car off the road because you were too focused on smoothing the bumps. Instead, build a vehicle that’s ready for the journey, no matter the terrain, low correlation to the rescue, ask for it!

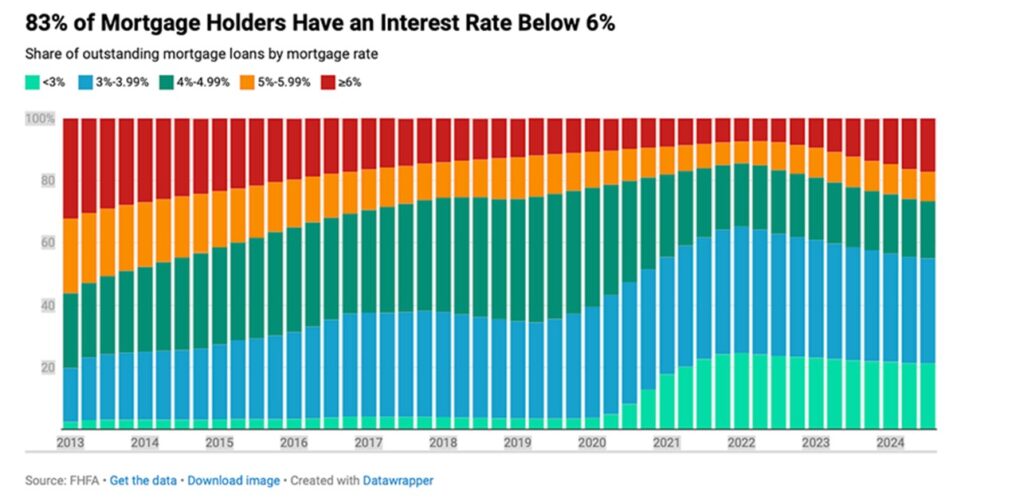

Data – Mortgage Rate Prison?

With today’s avg 30 yr rate about 7% but most owners at or below that, who would sell?

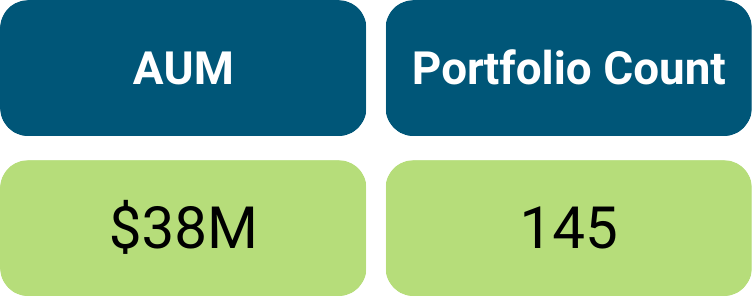

Data – AUM & Portfolio Count as of January 31, 2025

VCAFX and Portfolio News

1/31/2025 Fact card is posted on the website now.

We have closed on 3 new investments:

Abra – Charlotte, NC – an AI – Powered Vendor Intelligence Platform that combines contract terms, spend data, and stakeholder intelligence to optimize vendor spend and performance. CEO Byron would love to connect with you or anyone you may know who is interested a new approach to procurement.

Kigui – Mexico City, MX – optimizing supply chain management to help South American retailers better manage their inventory and reduce waste.

drypowder – Kansas City, MO – accounts receivable, payment automation, and operational management software for legacy industries like commodities and building materials.

NAV: You have seen the NAV grow (as of Valentine’s Day) to an all time high of $10.22. This price was achieved with help by some portfolio markups:

TCARE AI (Missouri), V360 (Kansas City), Scription AI (Alberta, Canada), and 1Fort AI (New York).

You can read more about those companies by hitting their weblinks above.

News:

While devastating fires swept across Los Angeles, our portfolio company Kommu demonstrated remarkable initiative in addressing a critical housing crisis. As thousands faced displacement, Kommu quickly pivoted their platform to launch a free centralized housing registry, bridging the gap between temporary relief measures and long-term housing needs. Unlike existing short-term solutions, Kommu focused on sustainable housing arrangements lasting months or longer essential for families facing extended rebuilding periods. Their platform actively monitors against price gouging and removes opportunistic brokers, ensuring fair rates for displaced residents. By creating a single, trusted source for housing listings and eliminating scattered spreadsheets and group chats, Kommu has streamlined the process of connecting local hosts with families in need. The company’s swift response and commitment to supporting LA’s long-term recovery exemplifies the kind of impact-driven innovation capable from a founder mindset.

Deal Flow: 220 YTD opportunities – this metric is on par with our expectations for this year. I expect this to grow over the coming weeks and months due to our recent activities in markets.

Availability: VCAFX is available for electronic trading on the following platforms: AXOS, SEI, Matrix, and Inspira. We have been given the go ahead for another name brand custody platform which should be on boarded in the next month and we have 6 others in our pipeline. VCAFX can also be purchased directly from our website at www.conneticvnetures.com/vcafx.

Most publicly available information is either on our website mentioned above, Morningstar.com or advisors can access our diligence information either from me or Banrion Capital Management.

The mention of specific securities should not be considered a recommendation. The specific securities identified and described herein do not represent all of the securities purchased or sold for the portfolio, and it should not be assumed that investment in these securities were or will be profitable. There is no assurance that the securities purchased remain in the portfolio or that securities sold have not been repurchased. For the top 10 holdings, please see the attached Fact Card.

Its tax and audit season at the home office, which is a super busy time. I have good news. Anyone needing K1s from the predecessor funds and LLCs, they are complete. 908 Investments LLC, the predecessor fund to VCAFX, is complete. Brian or Dawna has probably already reached out. Connetic Fund 1 LLC K1s are also ready. This is a 60 day improvement over 2024 delivery date (yes you can text me your happy faces!). There will be no 1099s for 2024 for VCAFX because we did not distribute any capital so all tax matters stay inside the fund unless distributed. Our focus right now is on the audit. I believe we are ahead of last year’s schedule, which makes sense as we are more experienced now and started the process a bit earlier. Big Kudo’s to our CFO, Brian McDermott, CPA® (yeah he’s got all the letters), as he makes this process as easy as it can be for us. I like to tell people when they ask me “how do you do this” I simply say “its magic”, well I can tell this group, Brian is the magic, so thank him if you talk to him. Personally, I have more travel coming up. I will be attending Future Proof in Miami in March and GOD willing, I will hopefully attend a sweet 16 NCAA tournament game with my daughter, Andie. It’s been 7 long years, so fingers crossed. I will probably squeeze in 1 more conference or road trip before the weather turns here and then take traveling break until the fall.

Last item: if you do NOT have online access yet, please take this as a nudge. Emailing me is the easiest way for me to help you, but its part of the magic being able to see your value move anyday you wish (plus you know you can add to your position online too!). Email: bzapp@conneticventures.com.

In closing, if you think you have a friend that may enjoy this newsletter, or getting to know us, please pass it along!

Kind regards,

Brad

Super Interesting Reads

- Kubera – Stay Ahead of your Wealth: Beyond the Stock Market

- Why Investors (and advisors) Fail: Why are we so foolish?

Thanks for reading!

We are pleased to partner with these companies to bring you this exciting newsletter.

This newsletter is sponsored by the companies shown above, whose logos and/or names appear as part of this communication. The sponsorship does not constitute an endorsement of any products, services, or investment opportunities mentioned herein. For more information about these companies, click on their logos.

For more information check out our Fact Card

Share using the buttons below

Follow Us

Some statements herein may express future expectations and forward-looking views based on Connetic’s current assumptions. Statements about companies, securities, or other financial information represent personal beliefs and viewpoints of Connetic or the respective third party. These statements may involve known and unknown risks and uncertainties, potentially leading to different results than those implied or expressed. All content is subject to change without notice.

The information herein was obtained from various sources. Connetic Ventures does not guarantee the accuracy or completeness of information provided by third parties. The information in this newsletter is given as of the date indicated and believed to be reliable. Connetic Ventures assumes no obligation to update this information, or to advise on further developments relating to it.

Connetic Ventures offers investment advisory services and is registered with the U.S. Securities and Exchange Commission (“SEC”). SEC registration does not constitute an endorsement of the advisory firm by the SEC nor does it indicate that the advisory firm has attained a particular level of skill or ability. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A & 2B can be obtained by visiting: https://adviserinfo.sec.gov and search for our firm name.

The Connetic Venture Capital Access Fund (the “Fund”) is a diversified, continuously offered, closed-end management investment company designed for long-term investors. The Fund is neither a liquid investment nor a trading vehicle. Connetic RIA LLC (the “Adviser” or “Connetic”) manages the Fund.

- Shares are not listed for trading on any securities exchange, and you should not expect to be able to sell Shares in a secondary market transaction. You should consider Shares of the Fund to be an illiquid investment.

- Shares are not redeemable at the shareholder’s option. The Fund does not intend to offer to repurchase Shares until January 2025. At that time, the Fund will offer to redeem no less than 5% of its outstanding Shares four times each year.

- The Fund has no intention to repurchase Shares outside of these quarterly repurchase offers that will begin in January 2025, and these repurchase offers may be oversubscribed.

- If you tender your Shares for repurchase as part of a repurchase offer that is oversubscribed (i.e., because more than 5% of the Fund’s outstanding Shares are tendered for repurchase), the Fund will redeem only a portion of your Shares.

- Because Shares are not listed on a securities exchange, and the Fund will only offer to redeem no less than 5% of its outstanding Shares four times a year starting in January 2025, you should not expect to be able to sell your Shares when and/or in the amount desired, regardless of how the Fund performs. As a result, you may be unable to reduce your exposure to the Fund during any market downturn.

- The Fund is designed for long-term investors. An investment in the Fund may not be suitable for you if you need the money you invest within a specified period.

- The amount of distributions the Fund may pay, if any, is uncertain. There is no assurance that the Fund will be able to maintain a certain level of distributions to shareholders. A portion or all of Fund distributions may consist of a return of capital. Any capital returned to shareholders through a distribution will be distributed after payment of fees and expenses. A return of capital distribution will not be taxable but will reduce the shareholder’s cost basis and result in a higher capital gain or lower capital loss when those shares on which the distribution was received are sold. Once a shareholder’s cost basis is reduced to zero, further distributions will be treated as capital gain if the shareholder holds shares of the Fund as capital assets.

- The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as from offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors.

- The Fund’s investments may require several years to appreciate in value, and there is no assurance that such appreciation will occur.

- Investing in the Shares may be speculative and involve a high degree of risk, including the risks associated with venture capital investing and the potential loss of your entire investment. See “Risks” in this prospectus.

Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectus contains this and other information about the Fund and can be obtained by calling 1-800-711-9164 or by visiting the Fund’s website at https://www.conneticventures.com. Please read the prospectus carefully before investing. All investments involve risks, and past performance is no guarantee of future results.

The Fund is distributed by Foreside Financial Services, LLC.

Connetic RIA, LLC, 910 Madison Ave, Covington, KY 41011