March 13, 2025

Hello there,

Welcome again to any newcomers!

This is our biweekly newsletter where we talk venture capital (VC), Connetic, data, and sometimes funny stuff. Hope you enjoy and read to the end!

Recently, Brad Zapp and I had the incredible opportunity to guest lecture at the University of Cincinnati, thanks to Tim Metzner—a fellow VC and entrepreneur—who teaches a class focused on building a venture capital fund from the ground up. The students spend the semester crafting their own fund concepts, culminating in a pitch at the end. It was energizing to see the next generation dive deep into the mechanics of venture capital. I covered portfolio construction and follow-on strategies, while Brad shared insights on fundraising for a fund and the nuances of different LP personas. It’s the kind of class I wish had been available when I was in college.

What stood out to me most is how universities are evolving beyond traditional entrepreneurship classes to also explore the venture capital side of the equation. It’s exciting to see this shift—it not only highlights the growing interest in private investing among students but also reinforces the staying power of venture capital as an asset class. At the same time, the experience underscored a challenge in higher education: while adjunct professors like Tim bring invaluable real-world expertise to the classroom, universities often struggle with outdated structures like tenure, limiting the flow of domain experts into these roles. As the demand for specialized, practical knowledge increases, colleges need to rethink how they attract and empower top talent to teach the next wave of entrepreneurs and investors.

In today’s update:

- Understanding the Performance of Early-Stage and Late-Stage VC

- Data: 35% of Adults Will Start Their Search with AI by 2027

- Venture News: AI Funding Surged in 2024

- Connetic Corner: Expanding Deal Flow – Wendal’s Salt Lake City Pitch Competition

- Super Interesting Reads:

- Secondaries Swell

- Supersonic Commercial Air Travel

- Duolingo Killed It’s Mascot

- Stuff That’s Weird AF

By: Chris Hjelm

Portfolio Manager

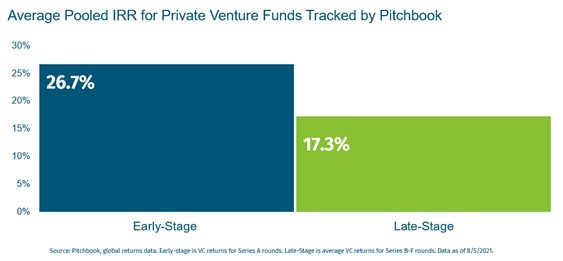

Understanding the Performance Gap Between Early and Late-Stage Venture Capital

Venture capital has long been an attractive, albeit complex, asset class for investors seeking outsized returns. Recent data from PitchBook, as of August 5, 2021, highlights a notable performance gap between early and late-stage VC investments. Early-stage funds, as defined by Pitchbook in this analysis, are those focusing on Series A and earlier rounds, have posted an average Internal Rate of Return (IRR) of 26.7%, significantly outpacing late-stage funds (Series B through Series F), which averaged a 17.3% IRR over the same period.

A Series A company typically has a proven product with early market traction, some initial revenue, and is focused on scaling its customer base and refining its business model. In contrast, companies in Series B through F rounds are more mature, with established revenue streams, expanded teams, and a focus on scaling operations, entering new markets, or preparing for an exit like an IPO or acquisition. While, these figures underscore the potential rewards of early-stage investing, it’s essential to remember that past performance does not guarantee future results.

One reason early-stage investments may outperform is the nature of venture capital’s power law return dynamics. In VC, a small percentage of portfolio companies typically generate the vast majority of returns. Early-stage investors gain access to startups at lower valuations, offering higher upside potential if a company becomes a market leader or achieves a significant exit. This approach, however, likely with higher risk—many early-stage companies fail to scale or secure follow-on funding. Yet, for well-constructed portfolios, the success of one or two outliers can more than compensate for losses, driving strong overall returns. Please see our prior newsletter from 10/17/2024 which discusses the VC power law.

Late-stage investing, while generally less volatile and tied to companies with established traction, often sees compressed returns due to higher entry valuations and increased competition among investors. Though this stage may offer more predictable exits and shorter time horizons, the trade-off is a lower ceiling for returns compared to early-stage opportunities. For financial advisors guiding clients in venture investing, understanding these dynamics is critical. Balancing potential upside with risk tolerance, time horizon, and diversification is key—especially in an asset class where a few standout investments can define the success of an entire portfolio.

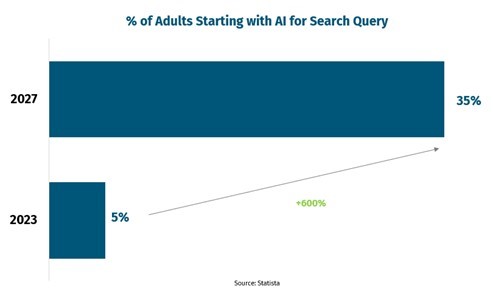

Data – 35% of Adults Will Start Their Search with AI by 2027

One of the most significant shifts in user behavior is happening right before our eyes—the move towards AI as the starting point for search. Data suggests that the percentage of people who begin their search journeys with AI platforms is set to grow from 5% in 2023 to an astonishing 35% by 2027. This isn’t just incremental change; it’s a seismic shift that could fundamentally disrupt the way we access information. For a company like Google, which derives the vast majority of its revenue from traditional search-based advertising, this trend poses a real threat to its core business. As more users turn to AI-driven tools that provide direct answers rather than a list of links, Google’s dominance—and its lucrative ad model—could be significantly impacted. I’ve personally felt this shift in my own habits. These days, I find myself starting nearly every search with an AI assistant. It’s faster, more intuitive, and often delivers exactly what I’m looking for without the noise. If this is happening at scale, we’re on the cusp of one of the biggest changes in the digital economy since the rise of Google itself.

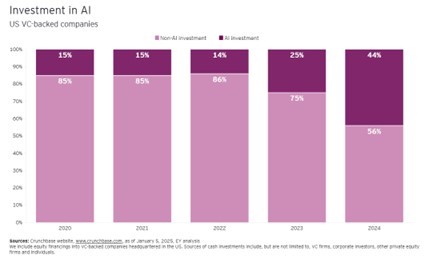

Venture News

AI continues to dominate VC funding with 44% of VC dollars going to AI companies in 2024.

Speaking of AI, I frequently bounce between different models especially during new releases or enhancements. Recently, I tried Grok 3, Elon’s latest model update and have to say it is the best LLM I have ever used. In my opinion, it is the most “human-like” and does not shy away from providing a strong POV which other models feel to do. Give it a try!

Expanding Deal Flow: Wendal’s Salt Lake City Pitch Competition

We recently returned from an exciting trip to Salt Lake City, where Wendal, our AI-driven deal sourcing platform, sponsored a pitch competition at one of the region’s largest tech conferences. This event was part of our ongoing initiative to tap into high-potential startup ecosystems that might otherwise fly under our radar. The competition offered a $200,000 investment to the winning startup, attracting a diverse range of early-stage companies eager to pitch.

The response was incredible—over 160 startups applied during the open application window. Using Wendal’s proprietary selection algorithms, we narrowed the pool down to five standout finalists, who then pitched live in front of a 500-person audience. This approach not only showcases some of the most promising startups in the area but also allows us to engage directly with ecosystems that are rich in talent yet often underrepresented in mainstream venture deal flow.

What makes these events so impactful is their efficiency in driving high-quality opportunities. On average, we invest in 1 out of every 70 startups that apply through Wendal. With over 160 applicants in Salt Lake City alone, this event exceeded our benchmarks, providing a pipeline of opportunities we wouldn’t have otherwise seen. It’s a win-win: startups gain exposure and funding, while we continue to diversify our portfolio with companies from vibrant but less tapped regions.

Super Interesting Reads

Thanks for reading!

We are pleased to partner with these companies to bring you this exciting newsletter.

This newsletter is sponsored by the companies shown above, whose logos and/or names appear as part of this communication. The sponsorship does not constitute an endorsement of any products, services, or investment opportunities mentioned herein. For more information about these companies, click on their logos.

For more information check out our Fact Card

Share using the buttons below

Follow Us

Some statements herein may express future expectations and forward-looking views based on Connetic’s current assumptions. Statements about companies, securities, or other financial information represent personal beliefs and viewpoints of Connetic or the respective third party. These statements may involve known and unknown risks and uncertainties, potentially leading to different results than those implied or expressed. All content is subject to change without notice.

The information herein was obtained from various sources. Connetic Ventures does not guarantee the accuracy or completeness of information provided by third parties. The information in this newsletter is given as of the date indicated and believed to be reliable. Connetic Ventures assumes no obligation to update this information, or to advise on further developments relating to it.

Connetic Ventures offers investment advisory services and is registered with the U.S. Securities and Exchange Commission (“SEC”). SEC registration does not constitute an endorsement of the advisory firm by the SEC nor does it indicate that the advisory firm has attained a particular level of skill or ability. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A & 2B can be obtained by visiting: https://adviserinfo.sec.gov and search for our firm name.

The Connetic Venture Capital Access Fund (the “Fund”) is a diversified, continuously offered, closed-end management investment company designed for long-term investors. The Fund is neither a liquid investment nor a trading vehicle. Connetic RIA LLC (the “Adviser” or “Connetic”) manages the Fund.

- Shares are not listed for trading on any securities exchange, and you should not expect to be able to sell Shares in a secondary market transaction. You should consider Shares of the Fund to be an illiquid investment.

- Shares are not redeemable at the shareholder’s option. The Fund does not intend to offer to repurchase Shares until January 2025. At that time, the Fund will offer to redeem no less than 5% of its outstanding Shares four times each year.

- The Fund has no intention to repurchase Shares outside of these quarterly repurchase offers that will begin in January 2025, and these repurchase offers may be oversubscribed.

- If you tender your Shares for repurchase as part of a repurchase offer that is oversubscribed (i.e., because more than 5% of the Fund’s outstanding Shares are tendered for repurchase), the Fund will redeem only a portion of your Shares.

- Because Shares are not listed on a securities exchange, and the Fund will only offer to redeem no less than 5% of its outstanding Shares four times a year starting in January 2025, you should not expect to be able to sell your Shares when and/or in the amount desired, regardless of how the Fund performs. As a result, you may be unable to reduce your exposure to the Fund during any market downturn.

- The Fund is designed for long-term investors. An investment in the Fund may not be suitable for you if you need the money you invest within a specified period.

- The amount of distributions the Fund may pay, if any, is uncertain. There is no assurance that the Fund will be able to maintain a certain level of distributions to shareholders. A portion or all of Fund distributions may consist of a return of capital. Any capital returned to shareholders through a distribution will be distributed after payment of fees and expenses. A return of capital distribution will not be taxable but will reduce the shareholder’s cost basis and result in a higher capital gain or lower capital loss when those shares on which the distribution was received are sold. Once a shareholder’s cost basis is reduced to zero, further distributions will be treated as capital gain if the shareholder holds shares of the Fund as capital assets.

- The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as from offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors.

- The Fund’s investments may require several years to appreciate in value, and there is no assurance that such appreciation will occur.

- Investing in the Shares may be speculative and involve a high degree of risk, including the risks associated with venture capital investing and the potential loss of your entire investment. See “Risks” in this prospectus.

Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectus contains this and other information about the Fund and can be obtained by calling 1-800-711-9164 or by visiting the Fund’s website at https://www.conneticventures.com. Please read the prospectus carefully before investing. All investments involve risks, and past performance is no guarantee of future results.

The Fund is distributed by Foreside Financial Services, LLC.

Connetic RIA, LLC, 910 Madison Ave, Covington, KY 41011